collapse and plm

Fast Transformation and Exploration of Panel Data

Sebastian Krantz

2021-06-27

Source:vignettes/collapse_and_plm.Rmd

collapse_and_plm.RmdThis vignette focuses on the integration of collapse and the popular plm (‘Linear Models for Panel Data’) package by Yves Croissant, Giovanni Millo and Kevin Tappe. It will demonstrate the utility of the pseries and pdata.frame classes introduced in plm together with the corresponding methods for fast collapse functions (implemented in C or C++), to extend and facilitate extremely fast computations on panel-vectors and panel data frames (20-100 times faster than native plm). The collapse package should enable R programmers to - with very little effort - write high-performance code in the domain of panel data exploration and panel data econometrics.

Notes:

To learn more about collapse, see the ‘Introduction to collapse’ vignette or the built-in structured documentation available under

help("collapse-documentation")after installing the package. In additionhelp("collapse-package")provides a compact set of examples for quick-start.Documentation and vignettes can also be viewed online.

The vignette is structured as follows:

Part 1 introduces collapse’s fast functions and associated transformation operators to compute various transformations on panel data, and delivers some benchmarks.

Part 2 uses these functions to explore panel data a bit and introduce additional functions for summary statistics, panel-autocorrelations and testing fixed effects.

Part 3 finally provides an example programming application by coding a slightly extended and very efficient Hausman and Taylor (1981) estimator.

For this vignette we will use a dataset (wlddev)

supplied with collapse containing a panel of 5 key development

indicators taken from the World Bank Development Indicators

Database:

library(collapse)

head(wlddev)

# country iso3c date year decade region income OECD PCGDP LIFEEX GINI ODA

# 1 Afghanistan AFG 1961-01-01 1960 1960 South Asia Low income FALSE NA 32.446 NA 116769997

# 2 Afghanistan AFG 1962-01-01 1961 1960 South Asia Low income FALSE NA 32.962 NA 232080002

# 3 Afghanistan AFG 1963-01-01 1962 1960 South Asia Low income FALSE NA 33.471 NA 112839996

# 4 Afghanistan AFG 1964-01-01 1963 1960 South Asia Low income FALSE NA 33.971 NA 237720001

# 5 Afghanistan AFG 1965-01-01 1964 1960 South Asia Low income FALSE NA 34.463 NA 295920013

# 6 Afghanistan AFG 1966-01-01 1965 1960 South Asia Low income FALSE NA 34.948 NA 341839996

# POP

# 1 8996973

# 2 9169410

# 3 9351441

# 4 9543205

# 5 9744781

# 6 9956320

fnobs(wlddev) # This column-wise counts the number of observations

# country iso3c date year decade region income OECD PCGDP LIFEEX GINI ODA

# 13176 13176 13176 13176 13176 13176 13176 13176 9470 11670 1744 8608

# POP

# 12919

fndistinct(wlddev) # This counts the number of distinct values

# country iso3c date year decade region income OECD PCGDP LIFEEX GINI ODA

# 216 216 61 61 7 7 4 2 9470 10548 368 7832

# POP

# 12877Part 1: Fast Transformation of Panel Data

First let us convert this data to a plm panel data.frame (class pdata.frame):

library(plm)

# This creates a panel data frame

pwlddev <- pdata.frame(wlddev, index = c("iso3c", "year"))

str(pwlddev, give.attr = FALSE)

# Classes 'pdata.frame' and 'data.frame': 13176 obs. of 13 variables:

# $ country: 'pseries' Named chr "Aruba" "Aruba" "Aruba" "Aruba" ...

# $ iso3c : Factor w/ 216 levels "ABW","AFG","AGO",..: 1 1 1 1 1 1 1 1 1 1 ...

# $ date : pseries, format: "1961-01-01" "1962-01-01" "1963-01-01" ...

# $ year : Factor w/ 61 levels "1960","1961",..: 1 2 3 4 5 6 7 8 9 10 ...

# $ decade : 'pseries' Named int 1960 1960 1960 1960 1960 1960 1960 1960 1960 1960 ...

# $ region : Factor w/ 7 levels "East Asia & Pacific",..: 3 3 3 3 3 3 3 3 3 3 ...

# $ income : Factor w/ 4 levels "High income",..: 1 1 1 1 1 1 1 1 1 1 ...

# $ OECD : 'pseries' Named logi FALSE FALSE FALSE FALSE FALSE FALSE ...

# $ PCGDP : 'pseries' Named num NA NA NA NA NA NA NA NA NA NA ...

# $ LIFEEX : 'pseries' Named num 65.7 66.1 66.4 66.8 67.1 ...

# $ GINI : 'pseries' Named num NA NA NA NA NA NA NA NA NA NA ...

# $ ODA : 'pseries' Named num NA NA NA NA NA NA NA NA NA NA ...

# $ POP : 'pseries' Named num 54211 55438 56225 56695 57032 ...

# A pdata.frame has an index attribute attached [retrieved using index(pwlddev) or attr(pwlddev, "index")]

str(index(pwlddev))

# Classes 'pindex' and 'data.frame': 13176 obs. of 2 variables:

# $ iso3c: Factor w/ 216 levels "ABW","AFG","AGO",..: 1 1 1 1 1 1 1 1 1 1 ...

# $ year : Factor w/ 61 levels "1960","1961",..: 1 2 3 4 5 6 7 8 9 10 ...

# This shows the individual and time dimensions

pdim(pwlddev)

# Balanced Panel: n = 216, T = 61, N = 13176A plm::pdata.frame is a data.frame with panel

identifiers attached as a list of factors in an index attribute

(non-factor index variables are converted to factor). Each column in

that data.frame is a Panel Series (plm::pseries), which

also has the panel identifiers attached:

# Panel Series of GDP per Capita and Life-Expectancy at Birth

PCGDP <- pwlddev$PCGDP

LIFEEX <- pwlddev$LIFEEX

str(LIFEEX)

# 'pseries' Named num [1:13176] 65.7 66.1 66.4 66.8 67.1 ...

# - attr(*, "names")= chr [1:13176] "ABW-1960" "ABW-1961" "ABW-1962" "ABW-1963" ...

# - attr(*, "index")=Classes 'pindex' and 'data.frame': 13176 obs. of 2 variables:

# ..$ iso3c: Factor w/ 216 levels "ABW","AFG","AGO",..: 1 1 1 1 1 1 1 1 1 1 ...

# ..$ year : Factor w/ 61 levels "1960","1961",..: 1 2 3 4 5 6 7 8 9 10 ...Now that we have explored the basic data structures provided in the plm package, let’s compute some transformations on them:

1.1 Between and Within Transformations

The functions fbetween and fbetween can be

used to compute efficient between and within transformations on panel

vectors and panel data.frames:

# Between-Transformations

head(fbetween(LIFEEX)) # Between individual (default)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 72.40653 72.40653 72.40653 72.40653 72.40653 72.40653

head(fbetween(LIFEEX, effect = "year")) # Between time

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 53.91206 54.47441 54.85718 55.20272 55.66802 56.12963

# Within-Transformations

head(fwithin(LIFEEX)) # Within individuals (default)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# -6.744533 -6.332533 -5.962533 -5.619533 -5.293533 -4.971533

head(fwithin(LIFEEX, effect = "year")) # Within time

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 11.74994 11.59959 11.58682 11.58428 11.44498 11.30537by default na.rm = TRUE thus both functions skip

(preserve) missing values in the data (which is the default for all

collapse functions). For fbetween the output

behavior can be altered with the option fill: Setting

fill = TRUE will compute the group-means on the complete

cases in each group (as long as na.rm = TRUE), but replace

all values in each group with the group mean (hence overwriting or

‘filling up’ missing values):

# This preserves missing values in the output

head(fbetween(PCGDP), 30)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965 ABW-1966 ABW-1967 ABW-1968 ABW-1969 ABW-1970

# NA NA NA NA NA NA NA NA NA NA NA

# ABW-1971 ABW-1972 ABW-1973 ABW-1974 ABW-1975 ABW-1976 ABW-1977 ABW-1978 ABW-1979 ABW-1980 ABW-1981

# NA NA NA NA NA NA NA NA NA NA NA

# ABW-1982 ABW-1983 ABW-1984 ABW-1985 ABW-1986 ABW-1987 ABW-1988 ABW-1989

# NA NA NA NA 25413.84 25413.84 25413.84 25413.84

# This replaces all individuals with the group mean

head(fbetween(PCGDP, fill = TRUE), 30)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965 ABW-1966 ABW-1967 ABW-1968 ABW-1969 ABW-1970

# 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84

# ABW-1971 ABW-1972 ABW-1973 ABW-1974 ABW-1975 ABW-1976 ABW-1977 ABW-1978 ABW-1979 ABW-1980 ABW-1981

# 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84

# ABW-1982 ABW-1983 ABW-1984 ABW-1985 ABW-1986 ABW-1987 ABW-1988 ABW-1989

# 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84 25413.84In fwithin the mean argument allows to set

an arbitrary data mean (different from 0) after the data is centered. In

grouped centering task, as sensible choice for such an added mean would

be the overall mean of the data series, enabled by the option

mean = "overall.mean". This will add the overall mean of

the series back to the data after subtracting out group means, and thus

preserve the level of the data (and will only change the intercept when

employed in a regression):

# This performed standard grouped centering

head(fwithin(LIFEEX))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# -6.744533 -6.332533 -5.962533 -5.619533 -5.293533 -4.971533

# This adds the overall average Life-Expectancy (across countries) to the country-demeaned series

head(fwithin(LIFEEX, mean = "overall.mean"))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 57.55177 57.96377 58.33377 58.67677 59.00277 59.32477fbetween and fwithin can also be applied to

pdata.frame’s where they will perform these computations

variable by variable:

head(fbetween(num_vars(pwlddev)), 3)

# decade PCGDP LIFEEX GINI ODA POP

# ABW-1960 1985.574 NA 72.40653 NA NA 76268.63

# ABW-1961 1985.574 NA 72.40653 NA NA 76268.63

# ABW-1962 1985.574 NA 72.40653 NA NA 76268.63

head(fbetween(num_vars(pwlddev), fill = TRUE), 3)

# decade PCGDP LIFEEX GINI ODA POP

# ABW-1960 1985.574 25413.84 72.40653 NA 33245000 76268.63

# ABW-1961 1985.574 25413.84 72.40653 NA 33245000 76268.63

# ABW-1962 1985.574 25413.84 72.40653 NA 33245000 76268.63

head(fwithin(num_vars(pwlddev)), 3)

# decade PCGDP LIFEEX GINI ODA POP

# ABW-1960 -25.57377 NA -6.744533 NA NA -22057.63

# ABW-1961 -25.57377 NA -6.332533 NA NA -20830.63

# ABW-1962 -25.57377 NA -5.962533 NA NA -20043.63

head(fwithin(num_vars(pwlddev), mean = "overall.mean"), 3)

# decade PCGDP LIFEEX GINI ODA POP

# ABW-1960 1960 NA 57.55177 NA NA 24223914

# ABW-1961 1960 NA 57.96377 NA NA 24225141

# ABW-1962 1960 NA 58.33377 NA NA 24225928Now next to fbetween and fwithin there also

exist short versions B and W, which are

referred to as transformation operators. These are essentially

wrappers around fbetween and fwithin and

provide the same functionality, but are more parsimonious to employ in

regression formulas and also offer additional features when applied to

panel data.frames. For panel series, B and W

are exact analogues to fbetween and fwithin,

just under a shorter name:

identical(fbetween(PCGDP), B(PCGDP))

# [1] TRUE

identical(fbetween(PCGDP, fill = TRUE), B(PCGDP, fill = TRUE))

# [1] TRUE

identical(fwithin(PCGDP), W(PCGDP))

# [1] TRUE

identical(fwithin(PCGDP, mean = "overall.mean"), W(PCGDP, mean = "overall.mean"))

# [1] TRUEWhen applied to panel data.frames, B and W

offer some additional utility by (a) allowing you to select columns to

transform using the cols argument (default is

cols = is.numeric, so by default all numeric columns will

be selected for transformation), (b) allowing you to add a prefix to the

transformed columns with the stub argument (default is

stub = "B." for B and stub = "W."

for W) and (c) preserving the panel-id’s with the

keep.ids argument (default

keep.ids = TRUE):

head(B(pwlddev), 3)

# iso3c year B.decade B.PCGDP B.LIFEEX B.GINI B.ODA B.POP

# ABW-1960 ABW 1960 1985.574 NA 72.40653 NA NA 76268.63

# ABW-1961 ABW 1961 1985.574 NA 72.40653 NA NA 76268.63

# ABW-1962 ABW 1962 1985.574 NA 72.40653 NA NA 76268.63

head(W(pwlddev, cols = 9:12), 3) # Here using the cols argument

# iso3c year W.PCGDP W.LIFEEX W.GINI W.ODA

# ABW-1960 ABW 1960 NA -6.744533 NA NA

# ABW-1961 ABW 1961 NA -6.332533 NA NA

# ABW-1962 ABW 1962 NA -5.962533 NA NAfbetween / B and fwithin /

W also support weighted computations. This of course

applies more to panel-survey settings, but for the sake of illustration

suppose we wanted to weight our between and within transformations by

the population of these countries:

# This replaces values by the POP-weighted group mean and also preserves the weight variable (POP, argument keep.w = TRUE)

head(B(pwlddev, w = ~ POP), 3)

# iso3c year POP B.decade B.PCGDP B.LIFEEX B.GINI B.ODA

# ABW-1960 ABW 1960 54211 1988.976 NA 72.96257 NA NA

# ABW-1961 ABW 1961 55438 1988.976 NA 72.96257 NA NA

# ABW-1962 ABW 1962 56225 1988.976 NA 72.96257 NA NA

# This centers values on the POP-weighted group mean

head(W(pwlddev, w = ~ POP, cols = c("PCGDP","LIFEEX","GINI")), 3)

# iso3c year POP W.PCGDP W.LIFEEX W.GINI

# ABW-1960 ABW 1960 54211 NA -7.300566 NA

# ABW-1961 ABW 1961 55438 NA -6.888566 NA

# ABW-1962 ABW 1962 56225 NA -6.518566 NA

# This centers values on the POP-weighted group mean and also adds the overall POP-weighted mean of the data

head(W(pwlddev, w = ~ POP, cols = c("PCGDP","LIFEEX","GINI"), mean = "overall.mean"), 3)

# iso3c year POP W.PCGDP W.LIFEEX W.GINI

# ABW-1960 ABW 1960 54211 NA 58.58012 NA

# ABW-1961 ABW 1961 55438 NA 58.99212 NA

# ABW-1962 ABW 1962 56225 NA 59.36212 NAAs shown above, with B and W the weight

column can also be passed as a formula or character string, whereas

fbetween and fwithin require the all inputs to

be passed directly in terms of data

(i.e. fbetween(get_vars(pwlddev, 9:11), w = pwlddev$POP)),

and the weight vector or id columns are never preserved in the output.

Therefore in most applications B and W are

probably more convenient for quick use, whereas fbetween

and fwithin are the preferred programmers choice, also

because they have a little less R-overhead which makes them a tiny bit

faster.

1.2 Higher-Dimensional Between and Within Transformations

Analogous to fbetween / B and

fwithin / W, collapse provides a duo

of functions and operators fhdbetween / HDB

and fhdwithin / HDW to efficiently average and

center data on multiple groups. The credit herefore goes to Laurent

Berge, the author of the fixest package who wrote an efficient

C-implementation of the alternating-projections algorithm to perform

this task. fhdbetween / HDB and

fhdwithin / HDW enrich this implementation

(available in the function fixest::demean) by providing

more options regarding missing values, and also allowing continuous

covariates and (full) interactions to be projected out alongside

factors. The methods for pseries and pdata.frame’s are

however rather simple, as they simply simultaneously center

panel-vectors on various panel-identifiers in the index (which can be

more than 2, the default is to center on all identifiers):

# This simultaneously averages Life-Expectancy across countries and years

head(HDB(LIFEEX)) # (same as running a regression on country and year dummies and taking the fitted values)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 62.36179 62.85981 63.24258 63.65245 64.11774 64.52503

# This simultaneously centers Life-Expectenacy on countries and years

head(HDW(LIFEEX)) # (same as running a regression on country and year dummies and taking the residuals)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 3.300210 3.214193 3.201424 3.134554 2.995255 2.909975The architecture of fhdbetween / HDB and

fhdwithin / HDW differs a bit from

fbetween / B and fwithin /

W. This is essentially a consequence of the underlying

C++-implementation (accessed through fixest::demean), which

was not built to accommodate missing values. fhdbetween /

HDB and fhdwithin / HDW therefore

both have an argument fill = TRUE (the default), which

stipulates that missing values in the data are preserved in the output.

The collapse default na.rm = TRUE again ensures

that only complete cases are used for the computation:

# Missing values are preserved in the output when fill = TRUE (the default)

head(HDB(PCGDP), 30)

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965 ABW-1966 ABW-1967 ABW-1968 ABW-1969 ABW-1970

# NA NA NA NA NA NA NA NA NA NA NA

# ABW-1971 ABW-1972 ABW-1973 ABW-1974 ABW-1975 ABW-1976 ABW-1977 ABW-1978 ABW-1979 ABW-1980 ABW-1981

# NA NA NA NA NA NA NA NA NA NA NA

# ABW-1982 ABW-1983 ABW-1984 ABW-1985 ABW-1986 ABW-1987 ABW-1988 ABW-1989

# NA NA NA NA 21833.32 22132.25 22479.20 22772.31

# When fill = FALSE, only the complete cases are returned

nofill <- HDB(PCGDP, fill = FALSE)

head(nofill, 30)

# ABW-1986 ABW-1987 ABW-1988 ABW-1989 ABW-1990 ABW-1991 ABW-1992 ABW-1993 ABW-1994 ABW-1995 ABW-1996

# 21833.32 22132.25 22479.20 22772.31 23064.29 23060.00 23089.75 23115.36 23343.25 23595.16 23823.11

# ABW-1997 ABW-1998 ABW-1999 ABW-2000 ABW-2001 ABW-2002 ABW-2003 ABW-2004 ABW-2005 ABW-2006 ABW-2007

# 24149.44 24424.69 24727.46 25205.98 25399.16 25603.11 25851.29 26349.64 26665.54 27224.58 27772.82

# ABW-2008 ABW-2009 ABW-2010 ABW-2011 ABW-2012 ABW-2013 ABW-2014 ABW-2015

# 27769.52 27002.95 27218.84 27424.18 27471.49 27660.92 27889.34 28107.78

# This results in a shorter panel-vector

length(nofill)

# [1] 9470

length(PCGDP)

# [1] 13176

# The cases that were missing and removed from the output are available as an attribute

head(attr(nofill, "na.rm"), 30)

# [1] 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 59 60 61 62In the pdata.frame methods there are 3 different choices how

to deal with missing values. The default for the plm classes in

variable.wise = TRUE, which will essentially sequentially

apply fhdbetween.pseries and fhdwithin.pseries

(with the default fill = TRUE) to all columns. This is the

same behavior as in fbetween / B and

fwithin / W, which also consider the

column-wise complete obs:

# This column-wise centers the data on countries and years

tail(HDW(pwlddev), 10)

# HDW.decade HDW.PCGDP HDW.LIFEEX HDW.GINI HDW.ODA HDW.POP

# ZWE-2011 0 -4632.971 -8.080748 -3.663217 118306300 -4547122

# ZWE-2012 0 -4523.505 -6.271385 NA 385526419 -4749368

# ZWE-2013 0 -4710.576 -4.753056 NA 149910333 -4903132

# ZWE-2014 0 -4931.693 -3.568136 NA 93295114 -5059317

# ZWE-2015 0 -5148.895 -2.685053 NA 150833589 -5224484

# ZWE-2016 0 -5433.809 -2.203219 NA -27844184 -5404667

# ZWE-2017 0 -5645.022 -1.920365 -1.964138 10266318 -5591762

# ZWE-2018 0 -5938.794 -1.759333 NA 59646823 -5774326

# ZWE-2019 0 -5710.646 -1.669415 5.627356 223473855 -5946725

# ZWE-2020 0 NA NA NA NA NAIf variable.wise = FALSE, fhdbetween /

HDB and fhdwithin / HDW will only

consider the complete cases in the dataset, but still return a dataset

of the same dimensions (as long as fill = TRUE), resulting

in some rows all-missing:

# This centers the complete cases of the data data on countries and years and keeps missing cases

tail(HDW(pwlddev, variable.wise = FALSE), 10)

# HDW.decade HDW.PCGDP HDW.LIFEEX HDW.GINI HDW.ODA HDW.POP

# ZWE-2011 0 517.6924 -4.379840 -3.839653 -176176494 -3042247

# ZWE-2012 NA NA NA NA NA NA

# ZWE-2013 NA NA NA NA NA NA

# ZWE-2014 NA NA NA NA NA NA

# ZWE-2015 NA NA NA NA NA NA

# ZWE-2016 NA NA NA NA NA NA

# ZWE-2017 0 -128.5240 1.971143 -1.314869 -67497466 1936716

# ZWE-2018 NA NA NA NA NA NA

# ZWE-2019 0 -389.1684 2.408697 5.154522 243673961 1105530

# ZWE-2020 NA NA NA NA NA NAFinally, if also fill = FALSE, the behavior is the same

as in the pseries method: Missing cases are removed from the

data:

# This centers the complete cases of the data data on countries and years, and removes missing cases

res <- HDW(pwlddev, fill = FALSE)

tail(res, 10)

# HDW.decade HDW.PCGDP HDW.LIFEEX HDW.GINI HDW.ODA HDW.POP

# ZMB-1996 0 534.39373 -3.6445256 -4.744748 -174237036 4911230.7

# ZMB-1998 0 201.58094 -4.1708951 -5.085621 -492258601 644947.7

# ZMB-2002 0 250.78234 -2.9085522 -10.912265 81848768 -1027712.3

# ZMB-2004 0 -72.94954 -1.9629513 1.494340 396830282 -3774596.6

# ZMB-2006 0 -308.55937 -0.4975872 2.407226 485998870 -2255101.6

# ZMB-2010 0 -428.16949 3.9600416 4.497547 -148714637 -4174306.2

# ZMB-2015 0 -1106.52213 8.4099983 7.553052 -335529320 -4962997.8

# ZWE-2011 0 517.69244 -4.3798401 -3.839653 -176176494 -3042246.9

# ZWE-2017 0 -128.52402 1.9711431 -1.314869 -67497466 1936716.5

# ZWE-2019 0 -389.16842 2.4086971 5.154522 243673961 1105530.5

tail(attr(res, "na.rm"))

# [1] 13169 13170 13171 13172 13174 13176Notes: (1) Because of the different missing case options

and associated challenges, panel-identifiers are not preserved in

HDB and HDW. (2) The default

variable.wise = TRUE and fill = TRUE was only

set for the pseries and pdata.frame methods, to

harmonize the default implementations with fbetween /

B and fwithin / W for these

classes. In the standard default, matrix and

data.frame methods, the defaults are

variable.wise = FALSE and fill = FALSE

(i.e. missing cases are removed beforehand), which is generally more

efficient.

1.3 Scaling and Centering

Next to the above functions for grouped centering and averaging, the

function / operator pair fscale / STD can be

used to efficiently standardize (i.e. scale and center) panel data along

an arbitrary dimension. The architecture is identical to that of

fwithin / W or fbetween /

B.

# This standardizes GDP per capita in each country

STD_PCGDP <- STD(PCGDP)

# Checks:

head(fmean(STD_PCGDP, index(STD_PCGDP, 1)))

# ABW AFG AGO ALB AND ARE

# -1.422473e-15 2.528841e-16 -6.189493e-16 -2.275957e-16 -9.281464e-16 -6.661338e-17

head(fsd(STD_PCGDP, index(STD_PCGDP, 1)))

# ABW AFG AGO ALB AND ARE

# 1 1 1 1 1 1

# This standardizes GDP per capita in each year

STD_PCGDP_T <- STD(PCGDP, effect = "year")

# Checks:

head(fmean(STD_PCGDP_T, index(STD_PCGDP_T, 2)))

# 1960 1961 1962 1963 1964 1965

# 9.882205e-17 3.496021e-16 1.889741e-17 -2.185013e-16 -1.724389e-16 2.616954e-16

head(fsd(STD_PCGDP_T, index(STD_PCGDP_T, 2)))

# 1960 1961 1962 1963 1964 1965

# 1 1 1 1 1 1And similarly for pdata.frame’s:

head(STD(pwlddev, cols = 9:12))

# iso3c year STD.PCGDP STD.LIFEEX STD.GINI STD.ODA

# ABW-1960 ABW 1960 NA -2.372636 NA NA

# ABW-1961 ABW 1961 NA -2.227700 NA NA

# ABW-1962 ABW 1962 NA -2.097539 NA NA

# ABW-1963 ABW 1963 NA -1.976876 NA NA

# ABW-1964 ABW 1964 NA -1.862193 NA NA

# ABW-1965 ABW 1965 NA -1.748918 NA NA

head(STD(pwlddev, cols = 9:12, effect = "year"))

# iso3c year STD.PCGDP STD.LIFEEX STD.GINI STD.ODA

# ABW-1960 ABW 1960 NA 0.9609854 NA NA

# ABW-1961 ABW 1961 NA 0.9485730 NA NA

# ABW-1962 ABW 1962 NA 0.9585105 NA NA

# ABW-1963 ABW 1963 NA 0.9669638 NA NA

# ABW-1964 ABW 1964 NA 0.9579477 NA NA

# ABW-1965 ABW 1965 NA 0.9556529 NA NAMore customized scaling can be done with the help of the

mean and sd arguments to fscale /

STD. By default mean = 0 and

sd = 1, but these could be assigned any numeric values:

# This will scale the data such that mean mean within each country is 5 and the standard deviation is 3

qsu(fscale(pwlddev$PCGDP, mean = 5, sd = 3))

# N/T Mean SD Min Max

# Overall 9466 5 2.968 -6.1908 16.257

# Between 202 5 0 5 5

# Within 46.8614 5 2.968 -6.1908 16.257Even further customization (i.e. setting means and standard

deviations for each group and / or each column) can of course be

achieved by calling collapse::TRA on the result of

fscale to sweep out an appropriate set of means and

standard deviations.

Scaling without centering can be done with the option

mean = FALSE. This will also preserve the mean of the data

overall and within each group:

# Scaling without centering: Mean preserving with fscale / STD

qsu(fscale(pwlddev$PCGDP, mean = FALSE, sd = 3))

# N/T Mean SD Min Max

# Overall 9466 12031.4627 17803.3537 247.7598 131349.27

# Between 202 12169.2793 18055.6626 253.1886 131342.669

# Within 46.8614 12031.4627 2.968 12020.2718 12042.7196

# Scaling without centering can also be done using fsd, but this does not preserve the mean

qsu(fsd(pwlddev$PCGDP, index(pwlddev, 1), TRA = "/"))

# N/T Mean SD Min Max

# Overall 9466 4.247 3.192 0.0579 26.647

# Between 202 4.6036 3.5846 0.8207 24.8111

# Within 46.8614 4.247 0.9893 0.5167 7.9993Finally a special kind of data harmonization in the first two moments

can be done by setting mean = "overall.mean" and

sd = "within.sd" in a grouped scaling task. This will

harmonize the data across groups such that the mean of each group is

equal to the overall data mean and the standard deviation equal to the

within standard deviation (= the standard deviation calculated on the

group-centered series):

fmean(pwlddev$PCGDP) # Overall mean

# [1] 12048.78

fsd(W(pwlddev$PCGDP)) # Within sd

# [1] 6723.681

# Scaling and centerin such that the mean of each country is the overall mean, and the sd of each country is the within sd

qsu(fscale(pwlddev$PCGDP, mean = "overall.mean", sd = "within.sd"))

# N/T Mean SD Min Max

# Overall 9466 12048.778 6651.9052 -13032.4333 37278.2175

# Between 202 12048.778 0 12048.778 12048.778

# Within 46.8614 12048.778 6651.9052 -13032.4333 37278.2175All of this seamlessly generalizes to weighted scaling an centering,

using the w argument to add a weight vector.

1.4 Panel Lags / Leads, Differences and Growth Rates

With flag / L / F,

fdiff / D and fgrowth /

G, collapse provides a fast and comprehensive C++

based solution to the computation of (sequences of) lags / leads and

(sequences of) lagged / leaded and suitably iterated (quasi-, log-)

differences and growth rates on panel data. The pseries and

pdata.frame methods to these functions and associated

transformation operators use the panel-identifiers in the

‘index’ attached to these objects (where the last variable in the

‘index’ is taken as the time-variable and the variables before that are

taken as individual identifiers) to perform fast fully-identified

time-dependent operations on panel data, without the need of sorting the

data.

With flag / L / F, it is easy

to lag or lead pseries:

# A panel-lag

head(flag(LIFEEX))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA 65.662 66.074 66.444 66.787 67.113

# A panel-lead

head(flag(LIFEEX, -1))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# 66.074 66.444 66.787 67.113 67.435 67.762

# The lag and lead operators are even more parsimonious to employ:

all_identical(L(LIFEEX), flag(LIFEEX), lag(LIFEEX))

# [1] TRUE

all_identical(F(LIFEEX), flag(LIFEEX, -1), lead(LIFEEX))

# [1] TRUEIt is also possible to compute a sequence of lags / leads using

flag or one of the operators:

# sequence of panel- lags and leads

head(flag(LIFEEX, -1:3))

# F1 -- L1 L2 L3

# ABW-1960 66.074 65.662 NA NA NA

# ABW-1961 66.444 66.074 65.662 NA NA

# ABW-1962 66.787 66.444 66.074 65.662 NA

# ABW-1963 67.113 66.787 66.444 66.074 65.662

# ABW-1964 67.435 67.113 66.787 66.444 66.074

# ABW-1965 67.762 67.435 67.113 66.787 66.444

all_identical(L(LIFEEX, -1:3), F(LIFEEX, 1:-3), flag(LIFEEX, -1:3))

# [1] TRUE

# The native plm implementation also returns a matrix of lags but with different column names

head(lag(LIFEEX, -1:3), 4)

# -1 0 1 2 3

# ABW-1960 66.074 65.662 NA NA NA

# ABW-1961 66.444 66.074 65.662 NA NA

# ABW-1962 66.787 66.444 66.074 65.662 NA

# ABW-1963 67.113 66.787 66.444 66.074 65.662Of course the lag orders may be unevenly spaced,

i.e. L(x, -1:3*12) would compute seasonal lags on monthly

data. On pdata.frame’s, the effects of flag and

L / F differ insofar that flag

will just lag the entire dataset without preserving identifiers

(although the index attribute is always preserved), whereas

L / F by default

(cols = is.numeric) select the numeric variables and add

the panel-id’s on the left (default keep.ids = TRUE):

# This lags the entire data

head(flag(pwlddev))

# country iso3c date year decade region income OECD PCGDP

# ABW-1960 <NA> <NA> <NA> <NA> NA <NA> <NA> NA NA

# ABW-1961 Aruba ABW 1961-01-01 1960 1960 Latin America & Caribbean High income FALSE NA

# ABW-1962 Aruba ABW 1962-01-01 1961 1960 Latin America & Caribbean High income FALSE NA

# ABW-1963 Aruba ABW 1963-01-01 1962 1960 Latin America & Caribbean High income FALSE NA

# ABW-1964 Aruba ABW 1964-01-01 1963 1960 Latin America & Caribbean High income FALSE NA

# ABW-1965 Aruba ABW 1965-01-01 1964 1960 Latin America & Caribbean High income FALSE NA

# LIFEEX GINI ODA POP

# ABW-1960 NA NA NA NA

# ABW-1961 65.662 NA NA 54211

# ABW-1962 66.074 NA NA 55438

# ABW-1963 66.444 NA NA 56225

# ABW-1964 66.787 NA NA 56695

# ABW-1965 67.113 NA NA 57032

# This lags only numeric columns and preserves panel-id's

head(L(pwlddev))

# iso3c year L1.decade L1.PCGDP L1.LIFEEX L1.GINI L1.ODA L1.POP

# ABW-1960 ABW 1960 NA NA NA NA NA NA

# ABW-1961 ABW 1961 1960 NA 65.662 NA NA 54211

# ABW-1962 ABW 1962 1960 NA 66.074 NA NA 55438

# ABW-1963 ABW 1963 1960 NA 66.444 NA NA 56225

# ABW-1964 ABW 1964 1960 NA 66.787 NA NA 56695

# ABW-1965 ABW 1965 1960 NA 67.113 NA NA 57032

# This lags only columns 9 through 12 and preserves panel-id's

head(L(pwlddev, cols = 9:12))

# iso3c year L1.PCGDP L1.LIFEEX L1.GINI L1.ODA

# ABW-1960 ABW 1960 NA NA NA NA

# ABW-1961 ABW 1961 NA 65.662 NA NA

# ABW-1962 ABW 1962 NA 66.074 NA NA

# ABW-1963 ABW 1963 NA 66.444 NA NA

# ABW-1964 ABW 1964 NA 66.787 NA NA

# ABW-1965 ABW 1965 NA 67.113 NA NAWe can also easily compute a sequence of lags / leads on a panel data.frame:

# This lags only columns 9 through 12 and preserves panel-id's

head(L(pwlddev, -1:3, cols = 9:12))

# iso3c year F1.PCGDP PCGDP L1.PCGDP L2.PCGDP L3.PCGDP F1.LIFEEX LIFEEX L1.LIFEEX L2.LIFEEX

# ABW-1960 ABW 1960 NA NA NA NA NA 66.074 65.662 NA NA

# ABW-1961 ABW 1961 NA NA NA NA NA 66.444 66.074 65.662 NA

# ABW-1962 ABW 1962 NA NA NA NA NA 66.787 66.444 66.074 65.662

# ABW-1963 ABW 1963 NA NA NA NA NA 67.113 66.787 66.444 66.074

# ABW-1964 ABW 1964 NA NA NA NA NA 67.435 67.113 66.787 66.444

# ABW-1965 ABW 1965 NA NA NA NA NA 67.762 67.435 67.113 66.787

# L3.LIFEEX F1.GINI GINI L1.GINI L2.GINI L3.GINI F1.ODA ODA L1.ODA L2.ODA L3.ODA

# ABW-1960 NA NA NA NA NA NA NA NA NA NA NA

# ABW-1961 NA NA NA NA NA NA NA NA NA NA NA

# ABW-1962 NA NA NA NA NA NA NA NA NA NA NA

# ABW-1963 65.662 NA NA NA NA NA NA NA NA NA NA

# ABW-1964 66.074 NA NA NA NA NA NA NA NA NA NA

# ABW-1965 66.444 NA NA NA NA NA NA NA NA NA NAEssentially the same functionality applies to fdiff /

D and fgrowth / G, with the main

differences that these functions also have a diff argument

to determine the number of iterations:

# Panel-difference of Life Expectancy

head(fdiff(LIFEEX))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA 0.412 0.370 0.343 0.326 0.322

# Second panel-difference

head(fdiff(LIFEEX, diff = 2))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA NA -0.042 -0.027 -0.017 -0.004

# Panel-growth rate of Life Expectancy

head(fgrowth(LIFEEX))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA 0.6274558 0.5599782 0.5162242 0.4881189 0.4797878

# Growth rate of growth rate of Life Expectancy

head(fgrowth(LIFEEX, diff = 2))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA NA -10.754153 -7.813521 -5.444387 -1.706782

identical(D(LIFEEX), fdiff(LIFEEX))

# [1] TRUE

identical(G(LIFEEX), fgrowth(LIFEEX))

# [1] TRUE

identical(fdiff(LIFEEX), diff(LIFEEX)) # Same as plm::diff.pseries (which does not compute iterated panel-differences)

# [1] TRUEBy default, growth rates are calculated in percentage terms which is

set by the default argument scale = 100. It is also

possible to compute log-differences with

fdiff(.., log = TRUE) or the Dlog operator,

and growth rates in percentage terms based on log-differences using

fgrowth(.., logdiff = TRUE).

# Panel log-difference of Life Expectancy

head(Dlog(LIFEEX))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA 0.006254955 0.005584162 0.005148963 0.004869315 0.004786405

# Panel log-difference growth rate (in percentage terms) of Life Expectancy

head(G(LIFEEX, logdiff = TRUE))

# ABW-1960 ABW-1961 ABW-1962 ABW-1963 ABW-1964 ABW-1965

# NA 0.6254955 0.5584162 0.5148963 0.4869315 0.4786405It is also possible to compute sequences of lagged / leaded and iterated differences, log-differences and growth rates:

# first and second forward-difference and first and second difference of lags 1-3 of Life-Expectancy

head(D(LIFEEX, -1:3, 1:2))

# FD1 FD2 -- D1 D2 L2D1 L2D2 L3D1 L3D2

# ABW-1960 -0.412 -0.042 65.662 NA NA NA NA NA NA

# ABW-1961 -0.370 -0.027 66.074 0.412 NA NA NA NA NA

# ABW-1962 -0.343 -0.017 66.444 0.370 -0.042 0.782 NA NA NA

# ABW-1963 -0.326 -0.004 66.787 0.343 -0.027 0.713 NA 1.125 NA

# ABW-1964 -0.322 0.005 67.113 0.326 -0.017 0.669 -0.113 1.039 NA

# ABW-1965 -0.327 0.006 67.435 0.322 -0.004 0.648 -0.065 0.991 NA

# Same with Log-differences

head(Dlog(LIFEEX, -1:3, 1:2))

# FDlog1 FDlog2 -- Dlog1 Dlog2 L2Dlog1 L2Dlog2

# ABW-1960 -0.006254955 -6.707929e-04 4.184520 NA NA NA NA

# ABW-1961 -0.005584162 -4.351984e-04 4.190775 0.006254955 NA NA NA

# ABW-1962 -0.005148963 -2.796481e-04 4.196359 0.005584162 -0.0006707929 0.01183912 NA

# ABW-1963 -0.004869315 -8.291000e-05 4.201508 0.005148963 -0.0004351984 0.01073312 NA

# ABW-1964 -0.004786405 5.098981e-05 4.206378 0.004869315 -0.0002796481 0.01001828 -0.001820838

# ABW-1965 -0.004837395 6.482830e-05 4.211164 0.004786405 -0.0000829100 0.00965572 -0.001077405

# L3Dlog1 L3Dlog2

# ABW-1960 NA NA

# ABW-1961 NA NA

# ABW-1962 NA NA

# ABW-1963 0.01698808 NA

# ABW-1964 0.01560244 NA

# ABW-1965 0.01480468 NA

# Same with (exact) growth rates

head(G(LIFEEX, -1:3, 1:2))

# FG1 FG2 -- G1 G2 L2G1 L2G2 L3G1 L3G2

# ABW-1960 -0.6235433 11.974895 65.662 NA NA NA NA NA NA

# ABW-1961 -0.5568599 8.428580 66.074 0.6274558 NA NA NA NA NA

# ABW-1962 -0.5135730 5.728297 66.444 0.5599782 -10.754153 1.1909476 NA NA NA

# ABW-1963 -0.4857479 1.727984 66.787 0.5162242 -7.813521 1.0790931 NA 1.713320 NA

# ABW-1964 -0.4774968 -1.051555 67.113 0.4881189 -5.444387 1.0068629 -15.45699 1.572479 NA

# ABW-1965 -0.4825714 -1.319230 67.435 0.4797878 -1.706782 0.9702487 -10.08666 1.491482 NAA further possibility is to compute quasi-differences and

quasi-log-differences of the form x_t - \rho

x_{t-s} or log(x_t) - \rho

log(x_{t-s}). These are useful for panel-regressions suffering

from serial-correlation, following Cochrane & Orcutt (1949), and can

be specified with the rho argument to fdiff,

D and Dlog.

# Regression of GDP on Life Expectance with country and time FE

mod <- lm(PCGDP ~ LIFEEX, data = fhdwithin(fselect(pwlddev, PCGDP, LIFEEX), fill = FALSE))

mod

#

# Call:

# lm(formula = PCGDP ~ LIFEEX, data = fhdwithin(fselect(pwlddev,

# PCGDP, LIFEEX), fill = FALSE))

#

# Coefficients:

# (Intercept) LIFEEX

# -2.442e-12 -3.330e+02

# Computing autocorrelation of residuals

r <- residuals(mod)

r <- pwcor(r, L(r, 1, substr(names(r), 1, 3))) # Need this to compute a panel-lag

r

# [1] .98

# Running the regression again quasi-differencing the transformed data

modCO <- lm(PCGDP ~ LIFEEX, data = fdiff(fhdwithin(fselect(pwlddev, PCGDP, LIFEEX), variable.wise = FALSE), rho = r, stubs = FALSE))

modCO

#

# Call:

# lm(formula = PCGDP ~ LIFEEX, data = fdiff(fhdwithin(fselect(pwlddev,

# PCGDP, LIFEEX), variable.wise = FALSE), rho = r, stubs = FALSE))

#

# Coefficients:

# (Intercept) LIFEEX

# -12.93 -91.97

# In this case rho is almost 1, so we might as well just difference the untransformed data and go with that

# We also need to bootstrap this for proper standard errors.A final important advantage of the collapse functions is that the panel-identifiers are preserved, even if a matrix of lags / leads / differences or growth rates is returned. This allows for nested panel-computations, for example we can compute shifted sequences of lagged / leaded and iterated panel differences:

# Sequence of differneces (same as above), adding one extra lag of the whole sequence

head(L(D(LIFEEX, -1:3, 1:2), 0:1))

# FD1 L1.FD1 FD2 L1.FD2 -- L1.-- D1 L1.D1 D2 L1.D2 L2D1 L1.L2D1 L2D2

# ABW-1960 -0.412 NA -0.042 NA 65.662 NA NA NA NA NA NA NA NA

# ABW-1961 -0.370 -0.412 -0.027 -0.042 66.074 65.662 0.412 NA NA NA NA NA NA

# ABW-1962 -0.343 -0.370 -0.017 -0.027 66.444 66.074 0.370 0.412 -0.042 NA 0.782 NA NA

# ABW-1963 -0.326 -0.343 -0.004 -0.017 66.787 66.444 0.343 0.370 -0.027 -0.042 0.713 0.782 NA

# ABW-1964 -0.322 -0.326 0.005 -0.004 67.113 66.787 0.326 0.343 -0.017 -0.027 0.669 0.713 -0.113

# ABW-1965 -0.327 -0.322 0.006 0.005 67.435 67.113 0.322 0.326 -0.004 -0.017 0.648 0.669 -0.065

# L1.L2D2 L3D1 L1.L3D1 L3D2 L1.L3D2

# ABW-1960 NA NA NA NA NA

# ABW-1961 NA NA NA NA NA

# ABW-1962 NA NA NA NA NA

# ABW-1963 NA 1.125 NA NA NA

# ABW-1964 NA 1.039 1.125 NA NA

# ABW-1965 -0.113 0.991 1.039 NA NAAll of this naturally generalized to computations on pdata.frames:

head(D(pwlddev, -1:3, 1:2, cols = 9:10), 3)

# iso3c year FD1.PCGDP FD2.PCGDP PCGDP D1.PCGDP D2.PCGDP L2D1.PCGDP L2D2.PCGDP L3D1.PCGDP

# ABW-1960 ABW 1960 NA NA NA NA NA NA NA NA

# ABW-1961 ABW 1961 NA NA NA NA NA NA NA NA

# ABW-1962 ABW 1962 NA NA NA NA NA NA NA NA

# L3D2.PCGDP FD1.LIFEEX FD2.LIFEEX LIFEEX D1.LIFEEX D2.LIFEEX L2D1.LIFEEX L2D2.LIFEEX

# ABW-1960 NA -0.412 -0.042 65.662 NA NA NA NA

# ABW-1961 NA -0.370 -0.027 66.074 0.412 NA NA NA

# ABW-1962 NA -0.343 -0.017 66.444 0.370 -0.042 0.782 NA

# L3D1.LIFEEX L3D2.LIFEEX

# ABW-1960 NA NA

# ABW-1961 NA NA

# ABW-1962 NA NA

head(L(D(pwlddev, -1:3, 1:2, cols = 9:10), 0:1), 3)

# iso3c year FD1.PCGDP L1.FD1.PCGDP FD2.PCGDP L1.FD2.PCGDP PCGDP L1.PCGDP D1.PCGDP

# ABW-1960 ABW 1960 NA NA NA NA NA NA NA

# ABW-1961 ABW 1961 NA NA NA NA NA NA NA

# ABW-1962 ABW 1962 NA NA NA NA NA NA NA

# L1.D1.PCGDP D2.PCGDP L1.D2.PCGDP L2D1.PCGDP L1.L2D1.PCGDP L2D2.PCGDP L1.L2D2.PCGDP

# ABW-1960 NA NA NA NA NA NA NA

# ABW-1961 NA NA NA NA NA NA NA

# ABW-1962 NA NA NA NA NA NA NA

# L3D1.PCGDP L1.L3D1.PCGDP L3D2.PCGDP L1.L3D2.PCGDP FD1.LIFEEX L1.FD1.LIFEEX FD2.LIFEEX

# ABW-1960 NA NA NA NA -0.412 NA -0.042

# ABW-1961 NA NA NA NA -0.370 -0.412 -0.027

# ABW-1962 NA NA NA NA -0.343 -0.370 -0.017

# L1.FD2.LIFEEX LIFEEX L1.LIFEEX D1.LIFEEX L1.D1.LIFEEX D2.LIFEEX L1.D2.LIFEEX L2D1.LIFEEX

# ABW-1960 NA 65.662 NA NA NA NA NA NA

# ABW-1961 -0.042 66.074 65.662 0.412 NA NA NA NA

# ABW-1962 -0.027 66.444 66.074 0.370 0.412 -0.042 NA 0.782

# L1.L2D1.LIFEEX L2D2.LIFEEX L1.L2D2.LIFEEX L3D1.LIFEEX L1.L3D1.LIFEEX L3D2.LIFEEX

# ABW-1960 NA NA NA NA NA NA

# ABW-1961 NA NA NA NA NA NA

# ABW-1962 NA NA NA NA NA NA

# L1.L3D2.LIFEEX

# ABW-1960 NA

# ABW-1961 NA

# ABW-1962 NA1.5 Panel Data to Array Conversions

Viewing and transforming panel data stored in an array can be a

powerful strategy, especially as it provides much more direct access to

the different dimensions of the data. The function psmat

can be used to efficiently transform pseries to a 2D matrix,

and pdata.frame’s to a 3D array:

# Converting the panel series to array, individual rows (default)

str(psmat(LIFEEX))

# 'psmat' num [1:216, 1:61] 65.7 32.4 37.5 62.3 NA ...

# - attr(*, "dimnames")=List of 2

# ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# - attr(*, "transpose")= logi FALSE

# Converting the panel series to array, individual columns

str(psmat(LIFEEX, transpose = TRUE))

# 'psmat' num [1:61, 1:216] 65.7 66.1 66.4 66.8 67.1 ...

# - attr(*, "dimnames")=List of 2

# ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# - attr(*, "transpose")= logi TRUE

# Same as plm::as.matrix.pseries, apart from attributes

identical(unattrib(psmat(LIFEEX)),

unattrib(as.matrix(LIFEEX)))

# [1] TRUE

identical(unattrib(psmat(LIFEEX, transpose = TRUE)),

unattrib(as.matrix(LIFEEX, idbyrow = FALSE)))

# [1] TRUEApplying psmat to a pdata.frame yields a 3D

array:

psar <- psmat(pwlddev, cols = 9:12)

str(psar)

# 'psmat' num [1:216, 1:61, 1:4] NA NA NA NA NA ...

# - attr(*, "dimnames")=List of 3

# ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..$ : chr [1:4] "PCGDP" "LIFEEX" "GINI" "ODA"

# - attr(*, "transpose")= logi FALSE

str(psmat(pwlddev, cols = 9:12, transpose = TRUE))

# 'psmat' num [1:61, 1:216, 1:4] NA NA NA NA NA NA NA NA NA NA ...

# - attr(*, "dimnames")=List of 3

# ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# ..$ : chr [1:4] "PCGDP" "LIFEEX" "GINI" "ODA"

# - attr(*, "transpose")= logi TRUEThis format can be very convenient to quickly and freely access data for different countries, variables and time-periods:

# Looking at wealth, health and inequality in Brazil and Argentinia, 1990-1999

aperm(psar[c("BRA","ARG"), as.character(1990:1999), c("PCGDP", "LIFEEX", "GINI")])

# , , BRA

#

# 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

# PCGDP 7983.7 7963.1 7791.8 8020.6 8311.6 8540.1 8591.0 8744.8 8641.3 8554.1

# LIFEEX 66.3 66.7 67.1 67.5 67.9 68.3 68.7 69.1 69.4 69.8

# GINI 60.5 NA 53.2 60.1 NA 59.6 59.9 59.8 59.6 59.0

#

# , , ARG

#

# 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

# PCGDP 6245.7 6721.3 7157.3 7644.2 7988.6 7666.5 7994.2 8543.0 8772.1 8381.3

# LIFEEX 71.6 71.8 72.0 72.2 72.5 72.7 72.8 73.0 73.2 73.4

# GINI NA 46.8 45.5 44.9 45.9 48.9 49.5 49.1 50.7 49.8psmat can also return the output as a list of panel

series matrices:

pslist <- psmat(pwlddev, cols = 9:12, array = FALSE)

str(pslist)

# List of 4

# $ PCGDP : 'psmat' num [1:216, 1:61] NA NA NA NA NA ...

# ..- attr(*, "dimnames")=List of 2

# .. ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# .. ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..- attr(*, "transpose")= logi FALSE

# $ LIFEEX: 'psmat' num [1:216, 1:61] 65.7 32.4 37.5 62.3 NA ...

# ..- attr(*, "dimnames")=List of 2

# .. ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# .. ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..- attr(*, "transpose")= logi FALSE

# $ GINI : 'psmat' num [1:216, 1:61] NA NA NA NA NA NA NA NA NA NA ...

# ..- attr(*, "dimnames")=List of 2

# .. ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# .. ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..- attr(*, "transpose")= logi FALSE

# $ ODA : 'psmat' num [1:216, 1:61] NA 116769997 -390000 NA NA ...

# ..- attr(*, "dimnames")=List of 2

# .. ..$ : chr [1:216] "ABW" "AFG" "AGO" "ALB" ...

# .. ..$ : chr [1:61] "1960" "1961" "1962" "1963" ...

# ..- attr(*, "transpose")= logi FALSEThis list can then be unlisted using the function

unlist2d (for unlisting in 2-dimensions), to yield a

reshaped data.frame:

head(unlist2d(pslist, idcols = "Variable", row.names = "Country Code"), 3)

# Variable Country Code 1960 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974

# 1 PCGDP ABW NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA

# 2 PCGDP AFG NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA

# 3 PCGDP AGO NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA

# 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986

# 1 NA NA NA NA NA NA NA NA NA NA NA 15669.616

# 2 NA NA NA NA NA NA NA NA NA NA NA NA

# 3 NA NA NA NA NA 3193.404 2947.194 2844.322 2859.919 2925.367 2922.217 2902.618

# 1987 1988 1989 1990 1991 1992 1993 1994 1995

# 1 18427.612 22134.017 24837.951 25357.787 26329.313 26401.969 26663.208 27272.310 26705.18

# 2 NA NA NA NA NA NA NA NA NA

# 3 2916.794 2989.617 2889.886 2697.491 2635.156 2401.234 1767.025 1733.844 1930.80

# 1996 1997 1998 1999 2000 2001 2002 2003 2004

# 1 26087.776 27190.501 27151.92 26954.40 28417.384 26966.055 25508.3027 25469.2876 27005.5294

# 2 NA NA NA NA NA NA 330.3036 343.0809 333.2167

# 3 2122.968 2205.294 2235.39 2211.13 2205.205 2223.335 2444.4178 2433.8616 2608.7840

# 2005 2006 2007 2008 2009 2010 2011 2012 2013

# 1 26979.8854 27046.2242 27427.579 27365.9312 24463.6922 23512.603 24233.0011 23781.2573 24635.7649

# 2 357.2347 365.2845 405.549 412.0143 488.3003 543.303 528.7366 576.1901 587.5651

# 3 2896.5547 3116.1810 3424.372 3668.0799 3565.0569 3587.884 3579.9599 3748.4507 3796.8822

# 2014 2015 2016 2017 2018 2019 2020

# 1 24563.2343 25822.2514 26231.0267 26630.2053 NA NA NA

# 2 583.6562 574.1841 571.0738 571.4407 564.610 573.2876 NA

# 3 3843.1979 3748.3201 3530.3107 3409.9303 3233.906 3111.1577 NAOf course we could also have applied some transformation (like computing pairwise correlations) to each matrix before unlisting. In any case this kind of programming provides lots of possibilities to explore and manipulate panel data (as we will see in Part 2).

Benchmarks

Below benchmarks are provided of the collapse implementation against native plm. To do this the dataset used so far is extended to have approx 1 million observations:

wlddevsmall <- get_vars(wlddev, c("iso3c","year","OECD","PCGDP","LIFEEX","GINI","ODA"))

wlddevsmall$iso3c <- as.character(wlddevsmall$iso3c)

data <- replicate(100, wlddevsmall, simplify = FALSE)

rm(wlddevsmall)

uniquify <- function(x, i) {

x$iso3c <- paste0(x$iso3c, i)

x

}

data <- unlist2d(Map(uniquify, data, as.list(1:100)), idcols = FALSE)

data <- pdata.frame(data, index = c("iso3c", "year"))

pdim(data)

# Balanced Panel: n = 21600, T = 61, N = 1317600The data has 21600 individuals (countries) observed for up to 61 years (1960-2020), the total number of rows is 1317600. We can pull out a series of life expectancy and run some benchmarks. The Windows laptop on which these benchmarks were run has a 2x 2.2 GHZ Intel i5 processor, 8GB DDR3 RAM and a Samsung SSD hard drive.

library(microbenchmark)

# Creating the extended panel series for Life Expectancy (l for large)

LIFEEX_l <- data$LIFEEX

str(LIFEEX_l)

# 'pseries' Named num [1:1317600] 65.7 66.1 66.4 66.8 67.1 ...

# - attr(*, "names")= chr [1:1317600] "ABW1-1960" "ABW1-1961" "ABW1-1962" "ABW1-1963" ...

# - attr(*, "index")=Classes 'pindex' and 'data.frame': 1317600 obs. of 2 variables:

# ..$ iso3c: Factor w/ 21600 levels "ABW1","ABW10",..: 1 1 1 1 1 1 1 1 1 1 ...

# ..$ year : Factor w/ 61 levels "1960","1961",..: 1 2 3 4 5 6 7 8 9 10 ...

# Between Transformations

microbenchmark(Between(LIFEEX_l, na.rm = TRUE), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# Between(LIFEEX_l, na.rm = TRUE) 17.73594 18.71248 21.84342 20.13574 22.35853 37.94689 10

microbenchmark(fbetween(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fbetween(LIFEEX_l) 4.408771 4.639519 4.705529 4.718424 4.771498 4.908684 10

# Within Transformations

microbenchmark(Within(LIFEEX_l, na.rm = TRUE), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# Within(LIFEEX_l, na.rm = TRUE) 10.17887 10.74663 10.91092 10.8766 11.24224 11.37664 10

microbenchmark(fwithin(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fwithin(LIFEEX_l) 4.522218 4.550303 4.735344 4.644296 4.696017 5.297036 10

# Higher-Dimenional Between and Within Transformations

microbenchmark(fhdbetween(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fhdbetween(LIFEEX_l) 56.916 57.29971 66.0179 58.13864 76.50108 84.10625 10

microbenchmark(fhdwithin(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fhdwithin(LIFEEX_l) 55.55906 56.2372 62.31852 56.56555 75.78784 77.20657 10

# Single Lag

microbenchmark(lag(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# lag(LIFEEX_l) 7.967776 8.144896 8.542879 8.632468 8.840092 8.949357 10

microbenchmark(flag(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# flag(LIFEEX_l) 7.994057 8.038747 8.337862 8.180484 8.603481 9.12086 10

# Sequence of Lags / Leads

microbenchmark(lag(LIFEEX_l, -1:3), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# lag(LIFEEX_l, -1:3) 18.7525 19.29476 28.61876 27.95813 38.11081 39.5329 10

microbenchmark(flag(LIFEEX_l, -1:3), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# flag(LIFEEX_l, -1:3) 15.5415 15.64335 21.10042 15.83998 33.37699 34.10265 10

# Single difference

microbenchmark(diff(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# diff(LIFEEX_l) 8.00525 8.16884 8.370421 8.368776 8.554404 8.733697 10

microbenchmark(fdiff(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(LIFEEX_l) 7.937805 8.020502 8.3458 8.2451 8.426238 9.34923 10

# Iterated Difference

microbenchmark(fdiff(LIFEEX_l, diff = 2), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(LIFEEX_l, diff = 2) 10.20129 10.62786 10.72184 10.77488 10.82326 11.21805 10

# Sequence of Lagged / Leaded and iterated differences

microbenchmark(fdiff(LIFEEX_l, -1:3, 1:2), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(LIFEEX_l, -1:3, 1:2) 45.90159 52.22494 66.83236 53.21347 57.53222 187.8582 10

# Single Growth Rate

microbenchmark(fgrowth(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fgrowth(LIFEEX_l) 8.222304 8.357153 8.69059 8.727158 8.884167 9.436683 10

# Single Log-Difference

microbenchmark(fdiff(LIFEEX_l, log = TRUE), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(LIFEEX_l, log = TRUE) 12.41394 12.8583 15.06961 13.17156 13.61659 32.51989 10

# Panel Series to Matrix Conversion

# system.time(as.matrix(LIFEEX_l)) This takes about 3 minutes to compute

microbenchmark(psmat(LIFEEX_l), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# psmat(LIFEEX_l) 1.482478 1.500149 1.628028 1.520813 1.553941 2.438639 10This shows a comparison between flag and data.table’s shift:

microbenchmark(L(data, cols = 3:6), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# L(data, cols = 3:6) 14.13692 14.43877 20.88276 18.865 19.73141 37.06244 10

library(data.table)

setDT(data)

# 'Improper' panel-lag

microbenchmark(data[, shift(.SD), by = iso3c, .SDcols = 3:6], times = 10)

# Unit: milliseconds

# expr min lq mean median uq max

# data[, shift(.SD), by = iso3c, .SDcols = 3:6] 176.5308 199.9415 215.6897 204.0719 230.089 268.9992

# neval

# 10

# This does what L is actually doing (without sorting the data)

microbenchmark(data[order(year), shift(.SD), by = iso3c, .SDcols = 3:6], times = 10)

# Unit: milliseconds

# expr min lq mean median

# data[order(year), shift(.SD), by = iso3c, .SDcols = 3:6] 193.9684 210.7025 213.7664 213.0727

# uq max neval

# 221.9783 226.3685 10The above dataset has 1 million obs in 20 thousand groups, but what about 10 million obs and 1 million groups? Do collapse functions scale efficiently as data and the number of groups grows large? Here is a simple benchmark:

x <- rnorm(1e7) # 10 million obs

g <- qF(rep(1:1e6, each = 10), na.exclude = FALSE) # 1 million individuals

t <- qF(rep(1:10, 1e6), na.exclude = FALSE) # 10 time-periods per individual

microbenchmark(fbetween(x, g), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fbetween(x, g) 51.66189 53.60693 91.00168 62.54655 73.87835 233.3696 10

microbenchmark(fwithin(x, g), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fwithin(x, g) 43.46291 44.03954 77.0216 45.33919 58.65132 196.7248 10

microbenchmark(flag(x, 1, g, t), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# flag(x, 1, g, t) 42.65382 55.05332 87.72527 59.55935 80.86143 210.8074 10

microbenchmark(flag(x, -1:1, g, t), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# flag(x, -1:1, g, t) 92.19842 92.5559 162.8994 166.736 228.6354 239.6953 10

microbenchmark(fdiff(x, 1, 1, g, t), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(x, 1, 1, g, t) 42.51778 46.29306 82.27838 53.85735 67.54295 205.0114 10

microbenchmark(fdiff(x, 1, 2, g, t), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(x, 1, 2, g, t) 59.9363 62.11689 84.42818 69.85072 75.38506 217.1431 10

microbenchmark(fdiff(x, -1:1, 1:2, g, t), times = 10)

# Unit: milliseconds

# expr min lq mean median uq max neval

# fdiff(x, -1:1, 1:2, g, t) 163.5046 182.9127 246.2855 250.664 301.4046 339.1415 10The results show that collapse functions perform very well even as the number of groups grows large.

The conclusion of this benchmark analysis is that collapse’s fast functions, with or without the help of plm classes, allow for very fast transformations of panel data, and should enable R programmers and econometricians to implement high-performance panel data estimators without having to dive into C/C++ themselves or resorting to data.table metaprogramming.

Part 2: Fast Exploration of Panel Data

collapse also provides some essential functions to summarize and explore panel data, such as a fast check of variation over different dimensions, fast summary-statistics for panel data, panel-auto, partial-auto and cross-correlation functions, and a fast F-test to test fixed effects and other exclusion restrictions on (large) panel data models. Panel data to matrix conversion further allows the application of some correlational and unsupervised learning tools such as PCA, clustering or dynamic factor analysis.

2.1 Variation Check for Panel Data

The function varying can be used to check over which

panel-dimensions different variable have variation. When passed a

pdata.frame, varying by default takes the first

identifier and checks for variation within that dimension.

# This checks for any variation within "iso3c", the first index variable: TRUE means data vary within country i.e. over time.

varying(pwlddev)

# country date year decade region income OECD PCGDP LIFEEX GINI ODA POP

# FALSE TRUE TRUE TRUE FALSE FALSE FALSE TRUE TRUE TRUE TRUE TRUEAlternatively any index variable or combination of index variables can be specified:

# This checks any variation within time variable, i.e. cross-sectional variation.

varying(pwlddev, effect = "year")

# country iso3c date decade region income OECD PCGDP LIFEEX GINI ODA POP

# TRUE TRUE FALSE FALSE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUEAnother possibility is checking for variation within each group:

# This checks cross-sectional variation within each year for 4 indicators.

head(varying(pwlddev, effect = "year", cols = 9:12, any_group = FALSE))

# PCGDP LIFEEX GINI ODA

# 1960 TRUE TRUE NA TRUE

# 1961 TRUE TRUE NA TRUE

# 1962 TRUE TRUE NA TRUE

# 1963 TRUE TRUE NA TRUE

# 1964 TRUE TRUE NA TRUE

# 1965 TRUE TRUE NA TRUEvarying also has a pseries method. The code below checks

for time-variation of the GINI index within each country. A

NA is returned when there are no observations within a

particular country.

head(varying(pwlddev$GINI, any_group = FALSE), 20)

# ABW AFG AGO ALB AND ARE ARG ARM ASM ATG AUS AUT AZE BDI BEL BEN BFA BGD BGR BHR

# NA NA TRUE TRUE NA TRUE TRUE TRUE NA NA TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE NAIf we would like to gave more information about this variation, we

could also invoke the functions fndistinct and

fsd, which do not have pseries methods:

head(fndistinct(pwlddev$GINI, index(pwlddev, "iso3c")), 20)

# ABW AFG AGO ALB AND ARE ARG ARM ASM ATG AUS AUT AZE BDI BEL BEN BFA BGD BGR BHR

# 0 0 3 9 0 2 29 20 0 0 9 16 5 4 16 3 5 9 12 0

head(round(fsd(pwlddev$GINI, index(pwlddev, "iso3c")), 2), 20)

# ABW AFG AGO ALB AND ARE ARG ARM ASM ATG AUS AUT AZE BDI BEL BEN BFA BGD BGR BHR

# NA NA 5.18 2.47 NA 4.60 3.84 2.76 NA NA 1.19 1.76 4.85 4.37 1.71 4.60 5.98 3.02 2.58 NA2.2 Summary Statistics for Panel Data

Efficient summary statistics for panel data have long been

implemented in other statistical softwares. The command

qsu, shorthand for ‘quick-summary’, is a very efficient

summary statistics command inspired by the xtsummarize command

in the Stata statistical software. It computes a default set of 5

statistics (N, mean, sd, min and max) and can also computed higher

moments (skewness and kurtosis) in a single pass through the data (using

a numerically stable online algorithm generalized from Welford’s

Algorithm for variance computations). With panel data, qsu

computes these statistics not just on the raw data, but also on the

between-transformed and within-transformed data:

qsu(pwlddev, cols = 9:12, higher = TRUE)

# , , PCGDP

#

# N/T Mean SD Min Max Skew Kurt

# Overall 9470 12048.778 19077.6416 132.0776 196061.417 3.1276 17.1154

# Between 206 12962.6054 20189.9007 253.1886 141200.38 3.1263 16.2299

# Within 45.9709 12048.778 6723.6808 -33504.8721 76767.5254 0.6576 17.2003

#

# , , LIFEEX

#

# N/T Mean SD Min Max Skew Kurt

# Overall 11670 64.2963 11.4764 18.907 85.4171 -0.6748 2.6718

# Between 207 64.9537 9.8936 40.9663 85.4171 -0.5012 2.1693

# Within 56.3768 64.2963 6.0842 32.9068 84.4198 -0.2643 3.7027

#

# , , GINI

#

# N/T Mean SD Min Max Skew Kurt

# Overall 1744 38.5341 9.2006 20.7 65.8 0.596 2.5329

# Between 167 39.4233 8.1356 24.8667 61.7143 0.5832 2.8256

# Within 10.4431 38.5341 2.9277 25.3917 55.3591 0.3263 5.3389

#

# , , ODA

#

# N/T Mean SD Min Max Skew Kurt

# Overall 8608 454'720131 868'712654 -997'679993 2.56715605e+10 6.9832 114.889

# Between 178 439'168412 569'049959 468717.916 3.62337432e+09 2.355 9.9487

# Within 48.3596 454'720131 650'709624 -2.44379420e+09 2.45610972e+10 9.6047 263.3716Key statistics to look at in this summary are the sample size and the

standard-deviation decomposed into the between-individuals and the

within-individuals standard-deviation: For GDP per Capita we have 8995

observations in the panel series for 203 countries, with on average

44.31 observations (time-periods T) per country. The between-country

standard deviation is 19600 USD, around 3-times larger than the

within-country (over-time) standard deviation of 6300 USD. Regarding the

mean, the between-mean, computed as a cross-sectional average of country

averages, usually differs slightly from the overall average taken across

all data points. The within-transformed data is computed and summarized

with the overall mean added back (i.e. as in

fwithin(PCGDP, mean = "overall.mean")).

We can also do groupwise panel-statistics and qsu also

supports weights (not shown):

qsu(pwlddev, ~ income, cols = 9:12, higher = TRUE)

# , , Overall, PCGDP

#

# N/T Mean SD Min Max Skew Kurt

# High income 3179 30280.7283 23847.0483 932.0417 196061.417 2.1702 10.3425

# Low income 1311 597.4053 288.4392 164.3366 1864.7925 1.2385 4.7115

# Lower middle income 2246 1574.2535 858.7183 144.9863 4818.1922 0.9093 3.7153

# Upper middle income 2734 4945.3258 2979.5609 132.0776 20532.9523 1.2286 4.9391

#

# , , Between, PCGDP

#

# N/T Mean SD Min Max Skew Kurt

# High income 71 30280.7283 20908.5323 5413.4495 141200.38 2.1347 9.9673

# Low income 28 597.4053 243.8219 253.1886 1357.3326 1.4171 5.3137

# Lower middle income 47 1574.2535 676.3157 444.2899 2896.8682 0.3562 2.2358

# Upper middle income 60 4945.3258 2327.3834 1604.595 13344.5423 1.24 4.7803

#

# , , Within, PCGDP

#

# N/T Mean SD Min Max Skew Kurt

# High income 44.7746 12048.778 11467.9987 -33504.8721 76767.5254 0.3924 6.0523

# Low income 46.8214 12048.778 154.1039 11606.2382 12698.296 0.5098 4.0676

# Lower middle income 47.7872 12048.778 529.1449 10377.7234 14603.1055 0.7658 5.4272

# Upper middle income 45.5667 12048.778 1860.395 4846.3834 24883.1246 0.6858 7.8469

#

# , , Overall, LIFEEX

#

# N/T Mean SD Min Max Skew Kurt

# High income 3831 73.6246 5.6693 42.672 85.4171 -1.0067 5.5553

# Low income 1800 49.7301 9.0944 26.172 74.43 0.2748 2.6721

# Lower middle income 2790 58.1481 9.3115 18.907 76.699 -0.3406 2.6845

# Upper middle income 3249 66.6466 7.537 36.535 80.279 -1.0988 4.2262

#

# , , Between, LIFEEX

#

# N/T Mean SD Min Max Skew Kurt

# High income 73 73.6246 3.3499 64.0302 85.4171 -0.6537 2.9946

# Low income 30 49.7301 4.8321 40.9663 66.945 1.5195 6.6802

# Lower middle income 47 58.1481 5.9945 45.7687 71.6078 0.0352 2.2126

# Upper middle income 57 66.6466 4.9955 48.057 74.0504 -1.3647 5.303

#

# , , Within, LIFEEX

#

# N/T Mean SD Min Max Skew Kurt

# High income 52.4795 64.2963 4.5738 42.9381 78.1271 -0.4838 3.8923

# Low income 60 64.2963 7.7045 41.5678 84.4198 0.0402 2.6086

# Lower middle income 59.3617 64.2963 7.1253 32.9068 83.9918 -0.2522 3.181

# Upper middle income 57 64.2963 5.6437 41.4342 83.0122 -0.507 4.0355

#

# , , Overall, GINI

#

# N/T Mean SD Min Max Skew Kurt

# High income 680 33.3037 6.7885 20.7 58.9 1.4864 5.6772

# Low income 107 41.1327 6.5767 29.5 65.8 0.7523 4.236

# Lower middle income 369 40.0504 9.3032 24 63.2 0.4388 2.2218

# Upper middle income 588 43.1585 8.9549 25.2 64.8 0.0814 2.3517

#

# , , Between, GINI

#

# N/T Mean SD Min Max Skew Kurt

# High income 41 33.3037 6.5238 24.8667 53.6296 1.5091 5.3913

# Low income 28 41.1327 5.1706 32.1333 58.75 0.6042 4.0473

# Lower middle income 46 40.0504 8.4622 27.6955 54.925 0.334 1.797

# Upper middle income 52 43.1585 8.4359 27.9545 61.7143 0.0336 2.2441

#

# , , Within, GINI

#

# N/T Mean SD Min Max Skew Kurt

# High income 16.5854 38.5341 1.8771 31.1841 45.8841 -0.0818 4.902

# Low income 3.8214 38.5341 4.0643 29.4591 55.3591 0.6766 5.1025

# Lower middle income 8.0217 38.5341 3.8654 27.9452 55.1008 0.4093 4.0058

# Upper middle income 11.3077 38.5341 3.0043 25.3917 48.0131 0.0728 3.5115

#

# , , Overall, ODA

#

# N/T Mean SD Min Max Skew

# High income 1575 153'663194 425'918409 -464'709991 4.34612988e+09 5.2505

# Low income 1692 631'660165 941'498380 -500000 1.04032100e+10 4.4628

# Lower middle income 2544 692'072692 1.02452490e+09 -605'969971 1.18790801e+10 3.7913

# Upper middle income 2797 301'326218 765'116131 -997'679993 2.56715605e+10 16.3123

# Kurt

# High income 36.2748

# Low income 32.1305

# Lower middle income 25.2442

# Upper middle income 464.8625

#

# , , Between, ODA

#

# N/T Mean SD Min Max Skew Kurt

# High income 42 153'663194 339'972909 468717.916 2.05456932e+09 3.9522 19.0792

# Low income 30 631'660165 466'265486 91'536334 1.67220583e+09 0.9769 2.6602

# Lower middle income 47 692'072692 765'003585 28'919000.2 3.62337432e+09 2.0429 7.2664

# Upper middle income 59 301'326218 382'148153 13'160000 1.91297800e+09 2.1072 7.0291

#

# , , Within, ODA

#

# N/T Mean SD Min Max Skew

# High income 37.5 454'720131 256'563661 -920'977647 2.87632242e+09 2.2074

# Low income 56.4 454'720131 817'933797 -1.19519570e+09 9.18572426e+09 3.8872

# Lower middle income 54.1277 454'720131 681'484247 -2.44379420e+09 1.12814455e+10 3.8965

# Upper middle income 47.4068 454'720131 662'846500 -2.04042108e+09 2.45610972e+10 19.6351

# Kurt

# High income 28.8682

# Low income 33.5194

# Lower middle income 47.7246

# Upper middle income 657.3041Here it should be noted that any grouping is applied independently from the data-transformation, i.e. the data is first transformed, and then grouped statistics are calculated on the transformed data. The computation of statistics is very efficient:

qsu(LIFEEX_l)

# N/T Mean SD Min Max

# Overall 1'167000 64.2963 11.4759 18.907 85.4171

# Between 20700 64.9537 9.87 40.9663 85.4171

# Within 56.3768 64.2963 6.0839 32.9068 84.4198

microbenchmark(qsu(LIFEEX_l))

# Unit: milliseconds

# expr min lq mean median uq max neval

# qsu(LIFEEX_l) 9.49355 10.25679 11.07317 10.37214 10.78839 50.22574 100Using the transformation functions and the functions

pwcor and pwcov, we can also easily explore

the correlation structure of the data:

# Overall pairwise correlations with pairwise observation count and significance testing (* = significant at 5% level)

pwcor(get_vars(pwlddev, 9:12), N = TRUE, P = TRUE)

# PCGDP LIFEEX GINI ODA

# PCGDP 1 (9470) .57* (9022) -.44* (1735) -.16* (7128)

# LIFEEX .57* (9022) 1 (11670) -.35* (1742) -.02 (8142)

# GINI -.44* (1735) -.35* (1742) 1 (1744) -.20* (1109)

# ODA -.16* (7128) -.02 (8142) -.20* (1109) 1 (8608)

# Between correlations

pwcor(fmean(get_vars(pwlddev, 9:12), pwlddev$iso3c), N = TRUE, P = TRUE)

# PCGDP LIFEEX GINI ODA

# PCGDP 1 (206) .60* (199) -.42* (165) -.25* (172)

# LIFEEX .60* (199) 1 (207) -.40* (165) -.21* (172)

# GINI -.42* (165) -.40* (165) 1 (167) -.19* (145)

# ODA -.25* (172) -.21* (172) -.19* (145) 1 (178)

# Within correlations

pwcor(W(pwlddev, cols = 9:12, keep.ids = FALSE), N = TRUE, P = TRUE)

# W.PCGDP W.LIFEEX W.GINI W.ODA

# W.PCGDP 1 (9470) .31* (9022) -.01 (1735) -.01 (7128)

# W.LIFEEX .31* (9022) 1 (11670) -.16* (1742) .17* (8142)

# W.GINI -.01 (1735) -.16* (1742) 1 (1744) -.08* (1109)

# W.ODA -.01 (7128) .17* (8142) -.08* (1109) 1 (8608)The correlations show that the between (cross-country) relationships of these macro-variables are quite strong, but within countries the relationships are much weaker, for example there seems to be no significant relationship between GDP per Capita and either inequality or ODA received within countries over time.

2.3 Exploring Panel Data in Matrix / Array Form

We can take a single panel series such as GDP per Capita and explore it further:

# Generating a (transposed) matrix of country GDPs per capita

tGDPmat <- psmat(PCGDP, transpose = TRUE)

tGDPmat[1:10, 1:10]

# ABW AFG AGO ALB AND ARE ARG ARM ASM ATG

# 1960 NA NA NA NA NA NA 5643 NA NA NA

# 1961 NA NA NA NA NA NA 5853 NA NA NA

# 1962 NA NA NA NA NA NA 5711 NA NA NA

# 1963 NA NA NA NA NA NA 5323 NA NA NA

# 1964 NA NA NA NA NA NA 5773 NA NA NA

# 1965 NA NA NA NA NA NA 6286 NA NA NA

# 1966 NA NA NA NA NA NA 6152 NA NA NA

# 1967 NA NA NA NA NA NA 6255 NA NA NA

# 1968 NA NA NA NA NA NA 6461 NA NA NA

# 1969 NA NA NA NA NA NA 6981 NA NA NA

# plot the matrix (it will plot correctly no matter how the matrix is transposed)

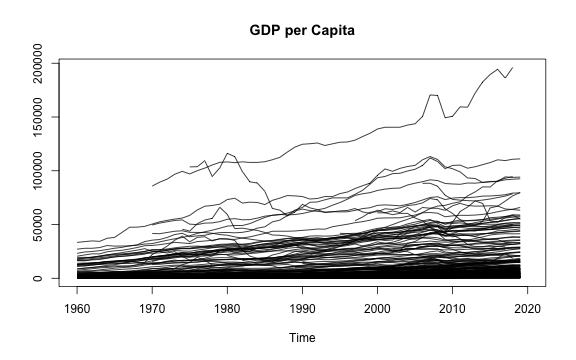

plot(tGDPmat, main = "GDP per Capita")

plot of chunk PLMGDPmat

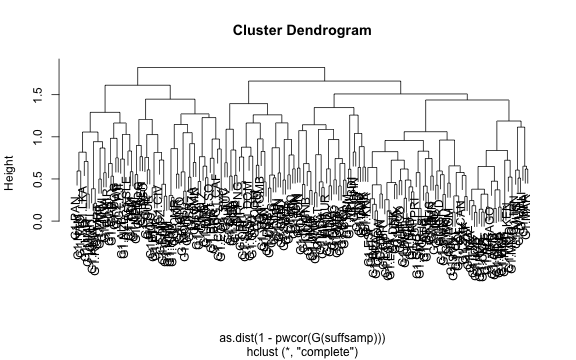

# Taking series with more than 20 observation

suffsamp <- tGDPmat[, fnobs(tGDPmat) > 20]

# Minimum pairwise observations between any two series:

min(pwnobs(suffsamp))

# [1] 16

# We can use the pairwise-correlations of the annual growth rates to hierarchically cluster the economies:

plot(hclust(as.dist(1-pwcor(G(suffsamp)))))

plot of chunk PLMGDPmat

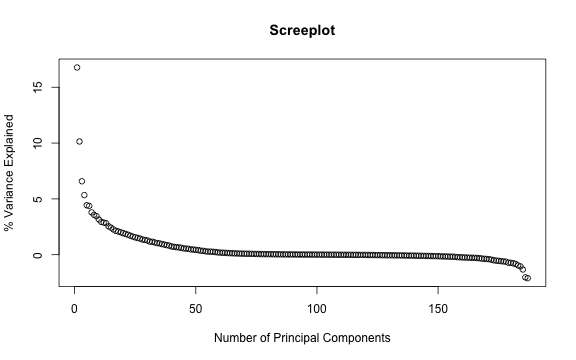

# Finally we could do PCA on the growth rates:

eig <- eigen(pwcor(G(suffsamp)))

plot(seq_col(suffsamp), eig$values/sum(eig$values)*100, xlab = "Number of Principal Components", ylab = "% Variance Explained", main = "Screeplot")

plot of chunk PLMGDPmat

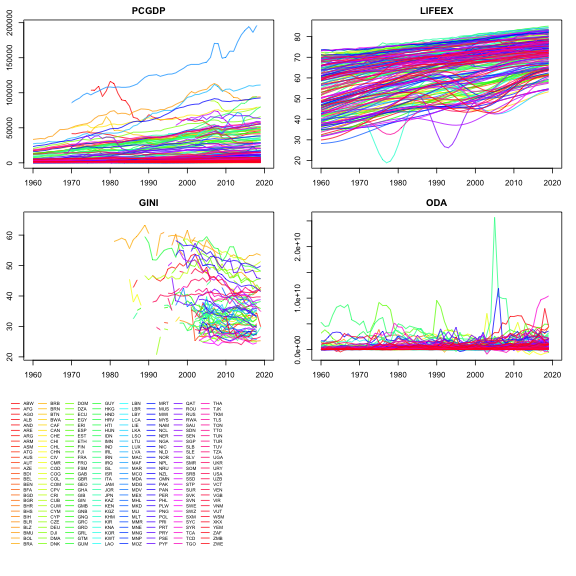

There is also a nice plot-method applied to panel series arrays

returned when psmat is applied to a panel data.frame:

plot of chunk pwlddev_plot

Above we have explored the cross-sectional relationship between the different national GDP series. Now we explore the time-dependence of the panel-vectors as a whole:

2.4 Panel- Auto-, Partial-Auto and Cross-Correlation Functions

The functions psacf, pspacf and

psccf mimic stats::acf,

stats::pacf and stats::ccf for panel-vectors

and panel data.frames. Below we compute the panel series autocorrelation

function of the data:

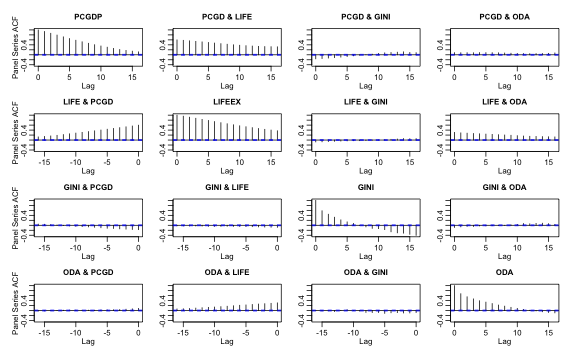

psacf(pwlddev, cols = 9:12)

plot of chunk plm_psacf

The computation is conducted by first scaling and centering

(i.e. standardizing) the panel-vectors by groups (using

fscale, default argument gscale = TRUE), and

then taking the covariance of each series with a matrix of properly

computed panel-lags of itself (using flag), and dividing

that by the variance of the overall series (using

fvar).

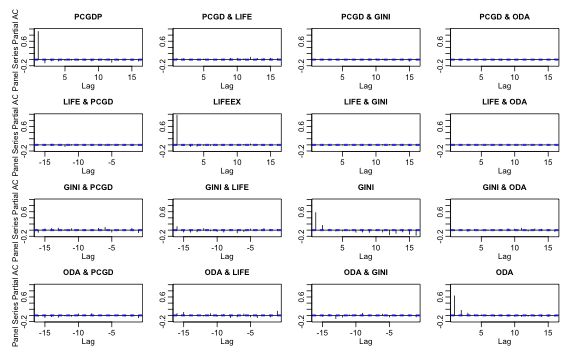

In a similar way we can compute the Partial-ACF (using a multivariate

Yule-Walker decomposition on the ACF, as in

stats::pacf),

pspacf(pwlddev, cols = 9:12)

plot of chunk plm_pspacf

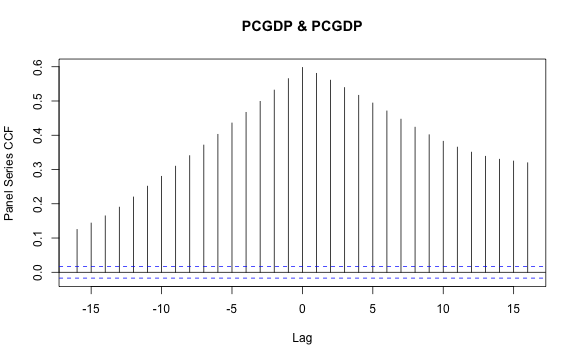

and the panel-cross-correlation function between GDP per capita and life expectancy (which is already contained in the ACF plot above):

psccf(PCGDP, LIFEEX)

plot of chunk plm_psccf

2.5 Testing for Individual Specific and Time-Effects

As a final step of exploration, we could analyze our series and

simple models for the significance and explanatory power of individual

or time-fixed effects, without going all the way to running a Hausman

Test of fixed vs. random effects on a fully specified model. The main

function here is fFtest which efficiently computes a fast

R-Squared based F-test of exclusion restrictions on models potentially

involving many factors. By default (argument

full.df = TRUE) the degrees of freedom of the test are

adjusted to make it identical to the F-statistic from regressing the

series on a set of country and time dummies1.

# Testing GDP per Capita

fFtest(PCGDP, index(PCGDP)) # Testing individual and time-fixed effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.905 264 9205 330.349 0.000

fFtest(PCGDP, index(PCGDP, 1)) # Testing individual effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.876 215 9254 303.476 0.000

fFtest(PCGDP, index(PCGDP, 2)) # Testing time effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.027 60 9409 4.276 0.000

# Same for Life-Expectancy

fFtest(LIFEEX, index(LIFEEX)) # Testing individual and time-fixed effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.924 265 11404 519.762 0.000

fFtest(LIFEEX, index(LIFEEX, 1)) # Testing individual effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.719 215 11454 136.276 0.000

fFtest(LIFEEX, index(LIFEEX, 2)) # Testing time effects

# R-Sq. DF1 DF2 F-Stat. P-value

# 0.218 60 11609 54.075 0.000Below we test the correlation between the country and time-means of GDP and Life-Expectancy:

cor.test(B(PCGDP), B(LIFEEX)) # Testing correlation of country means

#

# Pearson's product-moment correlation

#

# data: B(PCGDP) and B(LIFEEX)

# t = 78.752, df = 9020, p-value < 2.2e-16

# alternative hypothesis: true correlation is not equal to 0

# 95 percent confidence interval:

# 0.6259141 0.6503737

# sample estimates:

# cor

# 0.638305

cor.test(B(PCGDP, effect = 2), B(LIFEEX, effect = 2)) # Same for time-means

#

# Pearson's product-moment correlation

#

# data: B(PCGDP, effect = 2) and B(LIFEEX, effect = 2)

# t = 325.6, df = 9020, p-value < 2.2e-16

# alternative hypothesis: true correlation is not equal to 0

# 95 percent confidence interval:

# 0.9583431 0.9615804

# sample estimates:

# cor

# 0.9599938We can also test for the significance of individual and time-fixed effects (or both) in the regression of GDP on life expectancy and ODA received:

fFtest(PCGDP, index(PCGDP), get_vars(pwlddev, c("LIFEEX","ODA"))) # Testing individual and time-fixed effects

# R-Sq. DF1 DF2 F-Stat. P-Value

# Full Model 0.915 227 6682 316.551 0.000

# Restricted Model 0.162 2 6907 668.816 0.000

# Exclusion Rest. 0.753 225 6682 262.732 0.000

fFtest(PCGDP, index(PCGDP, 2), get_vars(pwlddev, c("iso3c","LIFEEX","ODA"))) # Testing time-fixed effects

# R-Sq. DF1 DF2 F-Stat. P-Value

# Full Model 0.915 227 6682 316.551 0.000

# Restricted Model 0.909 168 6741 403.168 0.000

# Exclusion Rest. 0.005 59 6682 7.238 0.000As can be expected in this cross-country data, individual and time-fixed effects play a large role in explaining the data, and these effects are correlated across series, suggesting that a fixed-effects model with both types of fixed-effects would be appropriate. To round things off, below we compute the Hausman test of Fixed vs. Random effects, which confirms this conclusion:

phtest(PCGDP ~ LIFEEX, data = pwlddev)

#

# Hausman Test

#

# data: PCGDP ~ LIFEEX

# chisq = 397.04, df = 1, p-value < 2.2e-16

# alternative hypothesis: one model is inconsistentPart 3: Programming Panel Data Estimators

A central goal of the collapse package is to facilitate advanced and fast programming with data. A primary field of application for the fast functions introduced above is to program efficient panel data estimators. In this section we walk through a short example of how this can be done. The application will be an implementation of the Hausman and Taylor (1981) estimator, considering a more general case than currently implemented in the plm package.

In Hausman and Taylor (1981), in a more general scenario, we have a linear panel-model of the form y_{it} = \beta_1X_{1it} + \beta_2X_{2it} + \beta_3Z_{1i} + \beta_4Z_{2i} + \alpha_i + \gamma_t + \epsilon where \alpha_i denotes unobserved individual specific effects and \gamma_t denotes unobserved global events. This model has up to 4 kinds of covariates:

Time-Varying covariates X_{1it} that are uncorrelated with the individual specific effect \alpha_i, such that E[X_{1it}\alpha_i] = 0. It may be the case that E[X_{1it}\gamma_t] \neq 0

Time-Varying covariates X_{2it} with E[X_{2it}\alpha_i] \neq 0 and possibly E[X_{2it}\gamma_t] \neq 0

Time-Invariant covariates Z_{1i} with E[Z_{1i}\alpha_i] = 0

Time-Invariant covariates Z_{2i} with E[Z_{2i}\alpha_i] \neq 0